This is the second entry in the Ledger — where Genesis gets tested against real systems. This one’s already scored.

What this is: A scored retrodiction—Genesis applied to Kodak at peak (1996), predictions checked against the known path to bankruptcy (2012)

Where the evidence lives: Center for Open Science

How it scored: 17/17 directional accuracy. Bet-level Brier: 0.050. Full scorecard published genesistheory.org/kodak.

How we know it wasn’t altered: The Seer registry on GitHub keeps scores hash-locked as SEER-2026-0002

In 1975, a 24-year-old electrical engineer at Kodak named Steve Sasson was given a minor assignment: see what you can do with this new chip called a charge-coupled device. Nobody asked him to build a camera. He built one anyway.

He scavenged a lens from a Super 8 movie camera, wired it to 16 nickel-cadmium batteries, an analog-to-digital converter, and several dozen circuits across six boards. The result weighed eight pounds.

It looked, as Sasson put it, like “a crazy-looking camera about the size of a toaster.” It captured a single black-and-white image—100 by 100 pixels—and took 23 seconds to record it onto a cassette tape.

He brought it to the executives. Took pictures of people in the room without explaining what he was doing. Then put the cassette in a playback unit and an image appeared on a television screen. That got their attention.

But the questions they asked weren’t how does it work? They asked: why would anyone want to take a picture this way when there’s nothing wrong with conventional photography?

“It was filmless photography,” Sasson told the New York Times years later, “so management’s reaction was, ‘that’s cute—but don’t tell anyone about it.’”

They patented the technology. Filed it away. And went back to selling film.

That moment didn’t break Kodak. In 1975, suppressing this “toaster with a lens” was rational—digital was a toy, film was an $8 billion market, and the company’s reading of its actual competitive landscape was accurate.

What the moment did was plant a reflex: deflect anything that disrupts the core business: film.

Over the next decade, that reflex hardened.

By the late 1980s, digital photography had moved from lab curiosity to commercial trajectory. Fuji was taking 2% of the US market share per year. And Kodak’s response was to file a WTO complaint rather than update its internal model.

By 1993, the gap between Kodak’s map and the territory it was supposed to describe had become structural—wide enough that even an outsider CEO, hired specifically to bridge it, got absorbed into the existing model rather than replacing it.

By 1996, the contradiction was fully load-bearing. Kodak reported $16 billion in revenue, $1.3 billion in profit, stock above $90, and the fifth most valuable brand in the world.

Wall Street rated it a buy. And Kodak’s own corporate literature simultaneously contained “roll film principles haven’t changed” and “digital is the greatest growth opportunity in the computer world.” Two contradictory maps, held at the same time, without resolution.

That’s not hedging. That’s a system that can no longer tell which of its own beliefs is true.

Running Genesis on Kodak

Before you test an instrument on a live patient, you test it on cases where the answer is known. Kodak is the known case. Everyone knows it went bankrupt in 2012. The question is whether Genesis can explain the mechanism—and whether it could have seen it coming from time-boxed data, when no one else did.

We ran the full Genesis protocol on evidence gathered restricted to pre-1997 data, diagnostic scoring, scenario construction, and prediction specification.

The same chain-of-custody as the Tesla forecast—claims feed the diagnostic, the diagnostic feeds the prediction, nothing gets invented downstream. The scored record is hash-locked in the Seer registry as SEER-2026-0002.

What Genesis saw

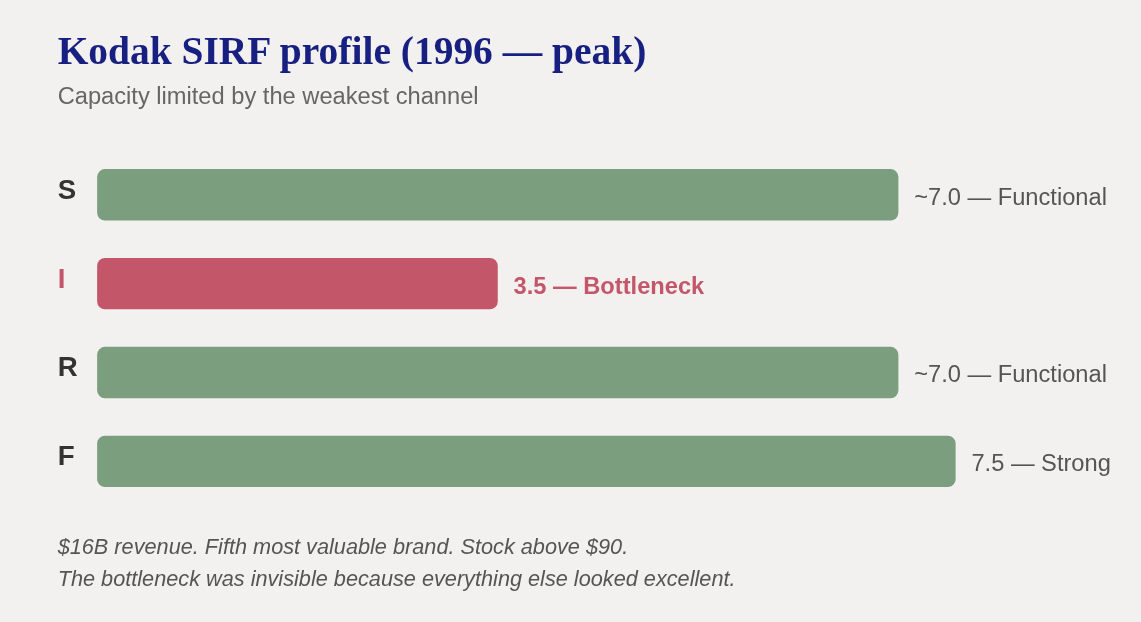

Genesis tracks four dimensions that any organized system needs to convert opportunity into results:

Structural—can it hold together?

Informational—can it see reality clearly?

Relational—do its key relationships help or hurt?

And Foundational—does it have the means and resources to act?

At peak, Kodak’s structure was functional, relationships were deep, and resources were strong (F = 7.5). But the information channel—the company’s ability to sense reality and correct course—scored 3.5. That’s the bottleneck. Capacity limited by the weakest channel.

Think about someone with talent, connections, and savings—but who can’t hear honest feedback. Friends try to explain why something isn’t working. This person deflects, rationalizes, and changes the subject. No amount of money helps. Their network can’t help.

Their one broken channel—the inability to take in accurate information—caps how much they can improve in this area.

That’s the bottleneck principle. Capacity gets limited by the weakest channel, not the strongest. Strength everywhere else doesn’t compensate—it funds the blind spot.

The Sasson moment was the seed. The late-1980s hardening to digital was the divergence. By 1996, the company held two incompatible models of its own future without recognizing the contradiction. Genesis calls this the model-reality divergence, expressed as:

Tis represents the gap between what the system believes and what’s actually happening.

At Kodak, 𝚫ϕ was large, persistent, and invisible to every conventional diagnostic because the financials looked excellent.

Three CEOS, three wrong maps

This is what most conventional frameworks fail to uncover.

Kodak didn’t fail because leadership was unaware of digital. Every CEO knew—and they had three of them churn during Kodak’s last run to bankruptcy. The failure was more specific: each leader read the situation, proposed a response, and got the same thing wrong.

George Fisher (1993–1999): protect film while investing in digital selectively. The old “both/and” strategy. Treated digital as a supplement to film, not a replacement. $5 billion invested across 23 fragmented projects—no unified digital strategy.

Dan Carp (2000–2005): pivot to digital. “Digital printing will replace film printing.” Updated the technology axis (film → digital) but not the economics axis. Assumed consumers would print digital photos at film-era margins. They didn’t—they shared on screens. More on this in a bit.

Antonio Perez (2005–2013): consumer inkjet printers with cheap ink. Updated again—but preserved the same core error. Photography had moved from atoms to bits. Every Kodak strategy tried to return it to physical atoms.

Three leaders. Three strategies. One invariant error: physical output equals value. The field moved to digital communication. Kodak’s map kept pointing back to printing.

Genesis predicted this pattern—from 1996—by measuring the correction rate (λ). Six documented events between 1975 and 1996 where reality pushed back and the company deflected or ignored.

The suppression reflex that started with Sasson’s demo had become institutional architecture by the late 1980s—and by 1996, the correction mechanism was so deeply compromised that even when the internal map finally updated, it updated incorrectly. The mechanism itself was damaged, not just delayed.

That’s why replacing the CEO didn’t fix it. The problem is organizational, not personal. Three CEOs tried, and three failed for the same structural reason.

The markets that closed (boundary walls)

While the internal diagnosis explains why Kodak couldn’t pivot, the boundary story explains what happened to the market it needed.

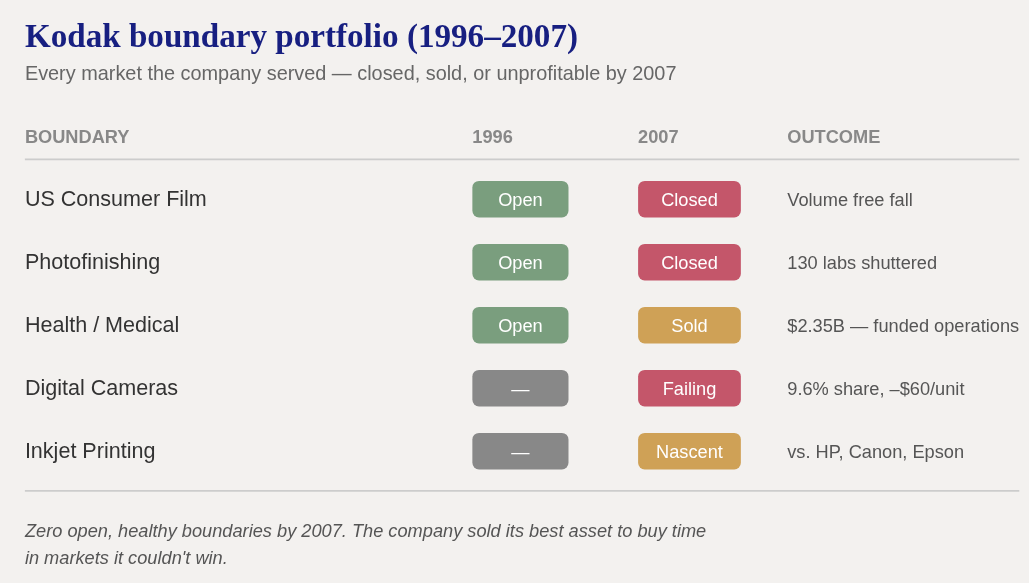

By 2007, eleven years after its peak, Kodak had zero open, healthy market boundaries.

US consumer film: closed (volume in free fall)

Photofinishing: closed (130 labs shuttered)

Health/medical imaging: sold for $2.35 billion to fund operations

Digital cameras: briefly opened, peaked at 21% share in 2005, collapsed to 9.6% by 2007—selling each unit at a $60 loss

Inkjet printing: entering a market dominated by HP, Canon, and Epson

The company sold its best remaining asset to buy time in markets it couldn’t win.

The boundary story mirrors the bottleneck story: the same broken reality-sensing that prevented internal correction also prevented recognizing which markets were closing and why. You can’t navigate to the right market if your map is wrong.

The timing trap

Kodak’s cash position (it’s F-channel) masked the severity—the same pattern we now see at Tesla.

At peak (1996), margin was healthy: 0.40. The company had a 10–15 year window to choose transformation. It spent seven of those years in resistance. Not because leadership was lazy, but because the margin was healthy enough to fund delay, and the broken correction mechanism prevented perceiving the urgency.

By 2003, margin had collapsed to 0.10. The window shrank to 3–5 years. And the resources needed to fund its transformation had been consumed by the delay itself.

This is the compounding trap: delay consumes the resources needed to act, which makes the eventual action more expensive, which consumes more resources. By the time cash pressure forces the pivot, the runway to execute it has already been spent.

Kodak’s dividend was slashed 72% in late 2003. That’s when the mode shift happened—not by choice, but by margin.

The company went from maintaining ➞ forced transformation ➞ survival.

By the time it filed for bankruptcy in January 2012, the $16 billion revenue machine had shrunk to $6.1 billion, with 145,000 employees reduced to 19,000.

Its 11,000 patents—including foundational digital imaging IP—sold for $525 million. What emerged was a $1 billion commercial printing company, a shell of its potential.

The scorecard

Every Genesis prediction scored against the known outcome.

We have two Brier scores because they measure different things.

The bet-level score (0.050) averages across all 17 individual predictions—each assigned probability against its binary outcome. Five times better than the no-skill baseline.

The scenario-level score (0.183) compares the base scenario probability (55%) against the aggregate forecast accuracy (0.978).

The gap between them signals that the structural diagnosis warranted higher confidence than the conservative 55% I initially assigned. In a first retrodiction with unvalidated methodology, conservatism is appropriate.

The two partial misses were both timing: non-viability predicted within 15 years (actual: 16), and workforce predicted below 15,000 by 2012 (actual: 19,000 at filing, below 8,000 post-emergence). No directional, structural, or mechanism errors.

For comparison:

Wall Street rated Kodak a buy at $90 and never predicted bankruptcy at any checkpoint.

McKinsey’s framework recommended the exact strategy that failed.

Christensen (RIP) correctly identified digital as a disruptive threat but couldn’t predict the specific failure mechanism, the self-repeating pivot pattern, the deferral timeline, or the cascade pathway.

Genesis forecasted all of these—from 1996 data.

Differential accuracy: +0.848 versus baseline frameworks.

What the retrodiction proves (and what it doesn’t)

The retrodiction demonstrates several things. The instrument can identify the binding constraint when conventional analysis can’t (I-channel, not Japanese competition).

It can predict that the same failure mode persists across CEO transitions (structural, not personnel). It can derive timing from margin analysis (the 5–7 year deferral prediction, nailed at exactly 7). And it can predict the specific direction of wrong pivots—atoms over bits—using field decomposition, which no baseline framework offers.

What it doesn’t prove: that the instrument works in real time. Retrodiction carries inherent 20/20 hindsight risk—however carefully you restrict evidence to pre-peak data, you can’t fully eliminate the possibility that knowing the ending influenced the diagnosis.

That’s why the Tesla prediction exists. Same instrument. Same protocol. Same chain-of-custody. But this time, the ending hasn’t happened yet. Seven predictions, all timestamped, all hash-locked, all resolving by December 2026.

Kodak calibrates this instrument. Tesla tests it. Resolution begins December 2026.

The pattern

One more thing. Kodak at peak and Tesla now share the same diagnostic profile—strong resources, broken reality-sensing, a correction rate frozen near zero, markets closing while leadership reads the clock that shows the most runway.

The mechanism differs (Kodak’s model-reality gap (𝚫ϕ) was technological, ironically its digital denial; Tesla’s is political and identity-driven boundary closure). But the physics is the same: cash can’t purchase model accuracy, and CEO replacement doesn’t fix structural model error.

Whether that pattern holds is exactly what the Tesla forecast tests.

Full materials: genesistheory.org/kodak

Registry: SEER-2026-0002

The Ledger: predictions, retrodictions, and calibration reviews. We publish the results either way. If you found this interesting, and would like to submit a prediction or a retrodiction similar to Kodak, email us at research@genesistheory.org.