Tesla’s real problem isn’t brand damage. It’s boundary closure.

A constraint-first gradable Tesla forecast (v1)—bets, falsifiers, and quarterly updates.

This is the first forecast in the Ledger—where Genesis gets tested against real systems. Predictions, retrodictions, and calibration reviews. We publish results regardless of outcome.

Start here:

What this is: A scored, timestamped forecast of Tesla Automotive through September 2026

Where the evidence lives: genesistheory.org/tesla-forecast

How it gets judged: Brier scoring + postmortems. Monthly monitoring. First scored results: October 2026

How we know it wasn’t altered: Seer registry—hash-locked before resolution

Why Tesla, why now

Genesis needed a prospective test case. Tesla Automotive fit the criteria:

Observable outcomes on a schedule. Quarterly deliveries, market share, regulatory actions—data arrives whether we like the results or not.

Conventional wisdom to test against. Wall Street consensus says brand headwinds, aging lineup, recovery with time and product. Genesis says something different.

Public evidence to run the protocol. SEC filings, earnings calls, third-party surveys, regulatory dockets. No insider access required.

So we ran it. Full protocol: evidence gathering, diagnostic scoring, scenario construction, prediction specification. The process generated three versioned documents, each tracing to the one before it. Claims feed the diagnostic. The diagnostic feeds the prediction. Nothing gets invented downstream.

That chain-of-custody matters—forecasting without evidence is just punditry with timestamps. Full materials at genesistheory.org/tesla-forecast: every claim ID, every scoring decision, every version change logged. The forecast itself is hash-locked in the Seer registry as SEER-2026-0003—any post-hoc modification is detectable.

The predictions

Most Tesla analysis follows a familiar script: brand headwinds from political controversy. Aging lineup needs refresh. Demand will recover with time and new product. Long-term autonomy story intact. Buy on weakness.

Genesis says something different. The problem isn’t damaged trust awaiting repair. It’s boundary closure—and closed boundaries don’t reopen.

Seven predictions. All probabilities assigned before resolution. All results published regardless of outcome.

Every claim has a date, a data source, and a way to prove us wrong. Resolution criteria, scoring methodology, and falsification details are in the evaluation plan.

Genesis uses the Brier score—0 is perfect, 0.25 is the no-skill baseline. The goal is to beat that baseline consistently and publish the results publicly.

Why this analysis differs

Most forecasting asks: What will happen?

Genesis asks: What’s still possible for this system—given its constraints—and will it update when reality disagrees?

That’s a different instrument, not just a different opinion.

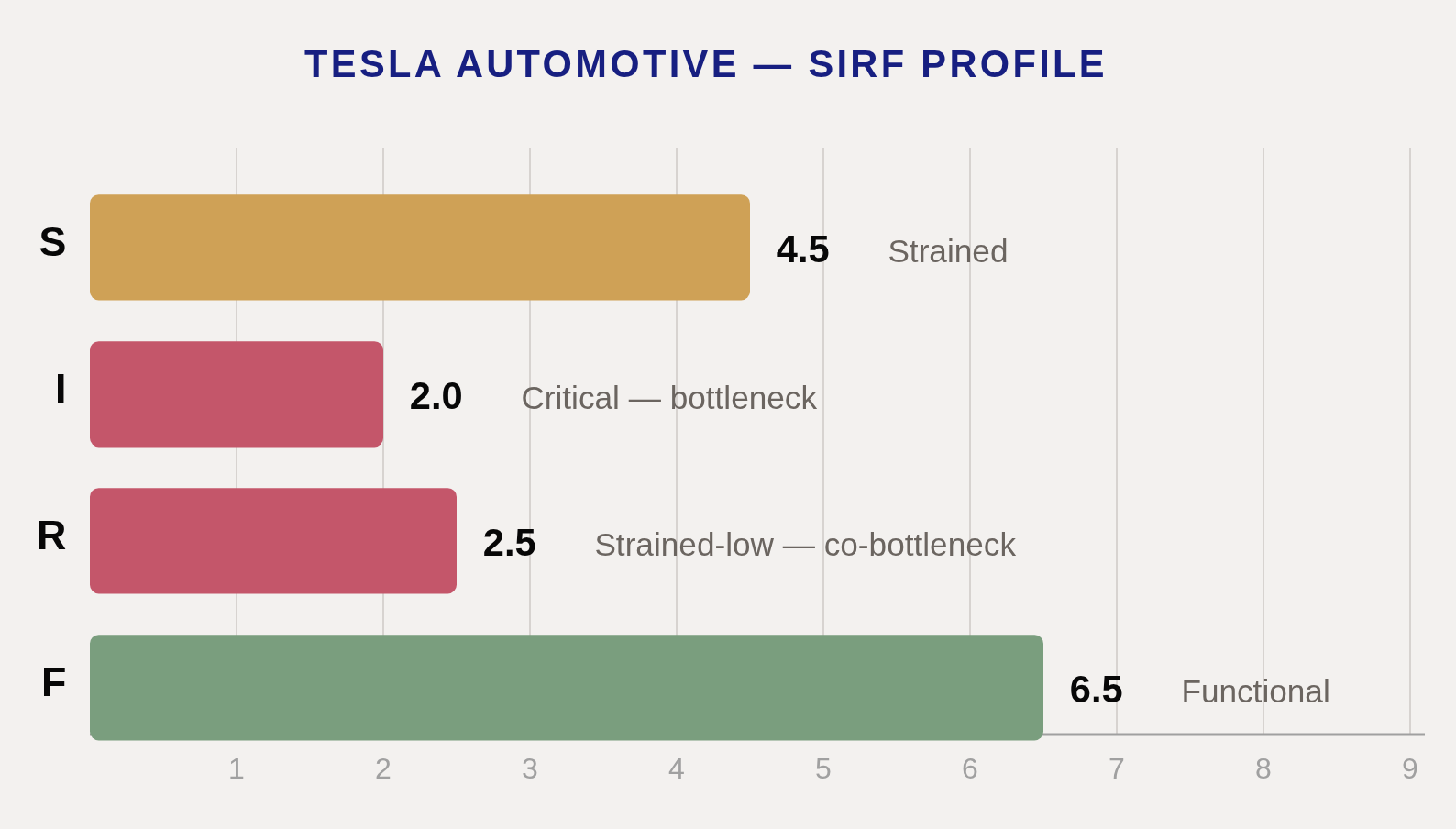

The capacity diagnosis

Genesis tracks four things any organized system needs to convert opportunity into results: structure (can it hold together?), information (can it see reality clearly?), relationships (do its key relationships help or hurt?), and resources (does it have the means to act?).

The bottleneck principle: capacity gets limited by the weakest channel.

Tesla’s profile:

Tesla’s bottleneck is I (information—reality-sensing), not F (resources). And R (relationships) has collapsed to meet it—forming a compound bottleneck. Both channels must improve for recovery to begin. The CEO causes both constraints.

Strong F doesn’t just fail to help—it obscures the severity. Cash funds operations, buys time, and signals resilience to investors. But it also funds bets the company’s broken reality-sensing can’t honestly evaluate: resources directed toward targets (robotaxi timelines, FSD deployment) that leadership can’t accurately scope because the correction mechanism is broken.

The $44B isn’t optionality. It’s runway for a company that can’t see where it’s headed.

We measure this with λ (lambda)—the system’s model-update rate.

Positive λ means the system corrects when wrong. Tesla’s λ is frozen near zero.

Nine years of FSD timeline misses without revision.

Robotaxi deployment 90% below target.

A court classified the CEO’s forward-looking statements as “corporate puffery.”

When reality pushes back, the pattern is doubles down, not updates.

The market diagnosis

That’s the capacity side. Now for the other half—what potential is available to convert?

Tesla’s addressable market contracted from ~2.0M units (2023) to ~1.14M (trajectory-adjusted 2026). A 43% decline in two years. Not a down cycle. Structural contraction through boundary closure.

The specific insight: conventional analysis treats brand erosion as a relationship problem—damaged trust, awaiting repair. Genesis treats much of it as something more permanent—segments that exited consideration entirely.

When a customer segment makes an identity decision (”I am not a Tesla buyer”), that’s not a relationship to repair. It’s a door that closed from the other side. No amount of product improvement, price reduction, or time reopens a door that closed on identity grounds.

In the US, Democratic buyer share dropped from 40% to 15%. An NBER study attributed 1.0–1.26 million lost sales to partisan effect.

In Europe, the same mechanism may be completing—sales fell 27.8% year-over-year, with Germany down 72% from peak.

The European rejection operates at civilizational scale: the perceived salute carries criminal prohibition in multiple countries where Tesla builds cars.

DOGE associated the CEO with an administration threatening trade war against European allies. The Sweden strike runs 29 months. These aren’t disconnected events. They’re a market approaching permanent boundary closure on identity grounds.

The CEO problem

The same leader who can’t see the problem internally also makes it worse externally—through political conduct, institutional destruction, and perceived hostility.

Our diagnostic audited the CEO's external conduct across six channels of activity operating at civilizational scale:

DOGE/political alignment

The perceived salute at the inauguration

The destruction of Twitter

EU legal proceedings

The Swedish strike and labor relations hostility.

Using cross-system comparison, we attribute roughly 55–60% of Tesla’s relational hostility to these navigator-driven emissions. They compound multiplicatively on the relationship channel with near-zero reversibility.

The environment isn’t hostile by coincidence. The CEO made it hostile—and continues making it more hostile, because the same frozen reality-sensing that prevents internal correction also prevents recognizing that his external conduct closes the markets the company needs.

The three clocks

Tesla’s leadership thinks they have five years. Our analysis says fifteen months. The cash says thirty.

The gap between these clocks is the finding. Tesla will lose its ability to choose transformation (the middle clock) well before it loses its ability to operate (the bottom clock). And leadership reads the clock that shows the most runway.

By the time cash pressure forces action, the window for chosen transformation has already closed.

The compounding dynamic

Broken reality-sensing and closing markets don’t just coexist. They reinforce each other:

Broken truth-sensing → Can’t see markets closing → Actions continue closing markets → Less opportunity available → Declining results → Narrative pivot (”AI company”) instead of correction → Reality-sensing stays broken → Loop continues.

The CEO sits at the center of this loop. His frozen correction rate locks the information channel. His external conduct poisons the relationship channel. His leadership architecture prevents anyone inside from breaking either. The company can’t correct because the dysfunction itself prevents recognizing the dysfunction.

What would prove us wrong

We pre-committed to these falsifiers before any resolution data. If any occur, specific parts of our analysis are wrong—and we’ll say so publicly. The full formal register is in the Seer forecast file.

Tesla publicly acknowledges brand damage as structural and announces remedial action → Leadership can sense and correct; reality-sensing is functional

2026 deliveries exceed 1.64M → Delivery decline was cyclical, not structural

European share holds above 8% every quarter through Q3 2026 → European rejection is cyclical, not identity-based

FSD achieves L3+ approval in any US jurisdiction by December 2026 → Regulatory relationship better than assessed

Cybercab production exceeds 25K in any quarter of 2026 → Production ramp constraint overstated

Brand loyalty recovers above 55% by September 2026 → Identity-based closure mechanism is wrong

Auto GM (ex-credits) exceeds 18% in any quarter through Q3 2026 → R→F cascade propagation thesis is wrong

Observable model-updating sustained 3+ months → Lambda can unfreeze; the triple trap can break from inside

The commitment

Genesis asks you to watch the test, not trust the theory blindly.

These are timestamped, hash-locked, falsifiable predictions. The Seer registry stores the specification, evidence, and forecast with SHA-256 hashes locked before any resolution data arrives. Anyone can verify.

If the predictions hit, the theory earns some credibility—building on the Kodak retrodiction that scored 0.050 Brier with 100% directional accuracy. If they miss, we’ll analyze why in public—measurement error, model error, or something the theory got wrong.

Full materials: genesistheory.org/tesla-forecast

Next update: April 2026, after Q1 delivery numbers. Subscribe to the Ledger to track whether this holds up.

The Ledger: predictions, retrodictions, and calibration reviews. We publish the results either way.